For many Americans afraid to lose their current low mortgage interest rate or compete in a tight housing market, home renovation may allow them to stay longer in their current home. But even though remodeling or upgrading your home may save you money over purchasing a new one, renovations can be expensive, especially with high material and labor costs.

While choosing to complete the renovations yourself or using lower quality materials can reduce costs, if the result isn’t professional, it may end up detracting from the value of your home. In this post we’ll offer our best tips on how to complete your renovation on a budget, avoiding spending pitfalls and utilizing interest-saving financing options. Keep reading to learn more about how to maximize your home improvement budget—without sacrificing quality in the process!

Create a Renovation Budget

Before you start your project, it’s important to examine your finances and create a renovation budget that not only adequately covers the cost of your project, but also fits into your financial picture. This includes creating a detailed budget, as well as making or updating a household budget, to help you see the true affordability of your plans.

Use Budgeting Tools to Make a Realistic Budget

Before you start making a budget for your project, it’s a good idea to have a general sense of what may be affordable for you. This will take into account any savings or cash funds you have to pay for your renovation, as well as room in your monthly budget for possible loan payments, if you also plan on seeking financing. If you don’t have a monthly budget, or haven’t revisited your budget in a while, take the time to make one.

Create a Monthly Budget

There are many ways to create a budget and spending plan, whether recording your expenses and income by hand using a graph paper and a pen, setting up a spreadsheet in a computer program like Excel, or using online tools like Peoples My Money Manager, available through Online and Mobile Banking, to automatically pull your spending and income data from your accounts.

Estimate Your Project Costs

After you have a general idea of your overall and monthly financial picture, you can start determining how much your project will cost. Estimating costs can be useful as you develop a ballpark budget, but—especially if you are using financing or have limited resources—it’s important to have a realistic, accurate budget, that includes 10-30% overages should costs rise (as they often do).

You can use online renovation resources like Angi’s Home Remodel Costs Estimator. It can be an excellent starting point to get a sense of how much things may cost. Additionally, ask friends, family, and neighbors who’ve recently completed home improvement projects for their costs by project, or on specifics like materials and labor.

Once you begin gathering estimates and shopping around for materials and fixtures, consider using a spreadsheet to keep track of your options and their prices.

Cut Costs to Stick to Your Budget

If you find that your desired renovation may be pushing your budget to the max, consider that there are many ways you can trim costs. Here are just a few things that can save you money.

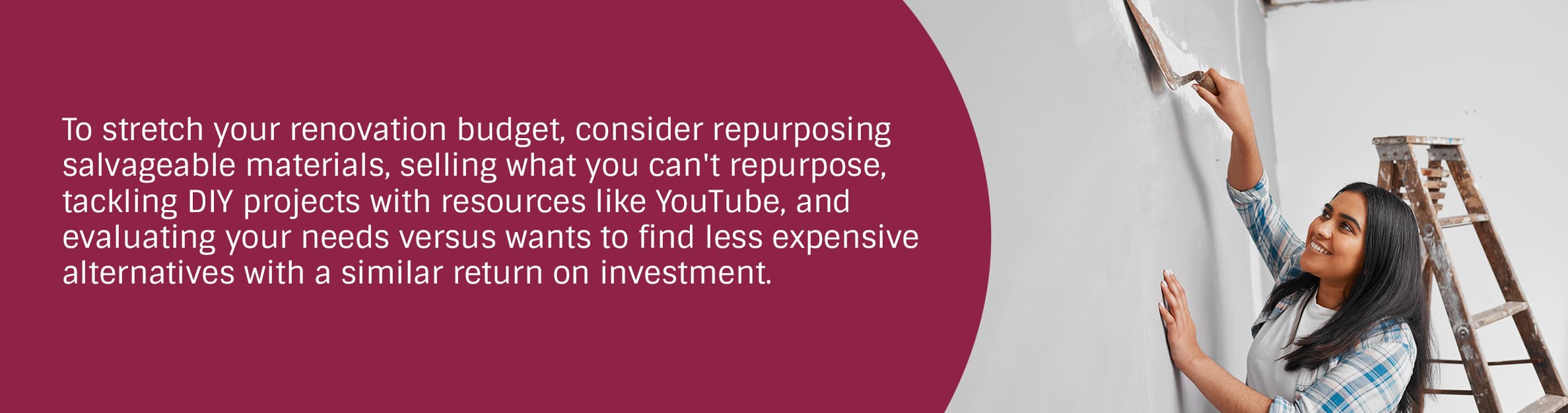

Reuse items where you can.

Before demolition, take inventory of what you can salvage to reuse or repurpose. For instance, quality kitchen cabinets in good condition can often be refinished or repainted, or even reused with new doors or hardware and new fixtures and a bit of elbow grease can revitalize an existing sink or tub.

Sell what you can’t reuse.

What you can’t repurpose, you can most likely sell. Items that may fetch a decent sum of money include copper piping, kitchen cabinets, furniture, brick, light fixtures, appliances, and flooring. And when your project is over, keep in mind you can often sell surplus tile, lumber, and other materials.

Partner with YouTube.

Demolition and painting are popular DIY options, but some other simple home improvements, including patching holes in drywall or even installing your own backsplash can be done with the help of a few instructional videos and a little bit of time. However, leave technical jobs to the professionals. Plumbing and electrical errors can be costly or dangerous, and poor workmanship can significantly detract from the value of your home.

Examine your needs versus your wants.

Some desirable high-ticket items, like marble countertops or expensive fixtures, often add less value to your home than they cost. Consider if you can achieve a similar look and return on investment with something less expensive? Many of the same principals you follow when narrowing down your needs vs. wants when buying a home can be applied to your renovation project, too.

Tips for Hiring a Contractor

Saving money on a home renovation doesn’t mean you need to cut corners or complete the entire project yourself. In fact, a quality renovation can add more value to your home than a haphazard or unprofessional job. For large, complex projects, it’s always worth the money to hire a professional—even if it may cost more. To make sure you get the most value for your dollar, keep these things in mind:

Know what you want and what you're willing to pay.

This is where having a budget and those initial cost estimates can be so important. Before you start negotiating with a contractor, make sure you know what you want and what you're willing to pay. While it may not be a good idea to share your maximum budget outright, communicating to a contractor if a bid is in line or high above your expectations and budget can help them work with you to select the scale project and types of materials that will allow you to maintain the affordability of your renovation. And having a clear understanding of your budget and priorities can also help you negotiate more effectively, should the estimate fall close, but moderately above your budget.

Get multiple bids.

Always get more than one bid for a project—at least three as a rule of thumb. Bids can vary significantly based on how much the contractor wants the job, how well the job fits into the contractor’s wheelhouse, or how close they are located to your home.

Beyond simply getting more than one bid, you may want to consider asking for a fixed-price proposal, in addition to an estimate, which often undercount costs by 5-20%. If your budget is firm or strictly limited by your financing, a fixed-price proposal can help avoid those surprise, budget-blowing additional charges. However, keep in mind that because fixed-price proposals usually include a contingency for overages, they may be higher than estimates.

Request a payment schedule.

While there are no specific laws detailing how much a contractor can expect you to pay upfront, to ensure that work for larger projects is fully completed, done on time, and the quality is up to your standards, it’s a good idea to insist on a set payment schedule. Ideal payment plans will require you to pay a percentage upfront (no more than 30% for big projects), with subsequent “draws” as critical stages are completed. And, as the South Dakota Office of Consumer Protection explains, never make the final payment until the following conditions are satisfied:

- All work meets the standards spelled out in the contract.

- You have written warranties for materials and workmanship.

- You have proof that all subcontractors and suppliers have been paid.

- The job site has been cleaned up and cleared of excess materials, tools, and equipment.

- You have inspected and approved the completed work.

Payment schedules give you greater control over the project, its costs, and its schedule, allow you to better monitor progress, and, most importantly, ensure that you aren’t left high and dry by an untrustworthy contractor.

Put everything in writing.

In addition to your payment schedule, you need to be sure that everything—from the scope of work to warranties and guarantees—is in writing in an official, legally-binding contract. In their publication, A Consumer's Guide to Hiring a Residential Building Contractor the Minnesota Department of Labor & Industry has a comprehensive list of things a solid, written contract should include. These include start and complete dates, payment schedule, building permit requirements, and payment holdback clauses.

Beyond your contract, be sure to write down any changes to the plan or special requests, to avoid disputes later on, and keep a clear record of payments. Rather than pay in cash, always pay with credit cards or checks, to have an official paper trail.

Be flexible.

As you are negotiating your contract, you may need to adjust your expectations. Be willing to be flexible on some aspects of the project, and expect some continuing supply chain and labor shortages. Know that some materials or design plans may simply be outside of your budget, and be willing to accept compromises. If you are working with a trusted and well-regarded contractor, they can guide you to make good decisions that allow you to satisfactorily complete your vision while keeping it affordable.

Financing Home Renovations: Options and Considerations

If you are putting off a major and necessary home renovation project because you are concerned about rising costs or interest rates, know that there are many financing options available that can use the equity in your home as collateral, enabling you to get the best interest rates. And if you’ve had your home for a few years, it has likely increased in value significantly.

A home equity loan or home equity line of credit (HELOC) can let you take advantage of this equity in your home, get lower interest rates than credit cards or unsecured personal loans, and even deduct the interest for home improvement projects from your federal taxes.

Home Equity Loans

A home equity loan is similar to a mortgage—in fact, home equity loans are often called “second mortgages.” With this kind of loan, you can receive a lump sum payment that is secured by your home equity. Because your home equity (the value of your home minus your mortgage balance) secures the loan, you can only receive a loan of up to 80% of your equity. Home equity loans are best used for projects with relatively fixed costs and completion times. If you aren’t sure how much your renovation will cost, rather than overestimate your loan, it may make more sense to use a home equity line of credit (more on these below).

Home equity loans usually have fixed interest rates, and come with set, monthly payments based on the amount you borrow and the length of your loan term, which can be anywhere from 5 to 18 years. Even if you don’t need to use all your funds up front, you will be required to pay interest and make payments as soon as your loan closes. Additionally, home equity loans have closing costs, which can be paid upfront or often rolled into the loan. Though less than first mortgages, they can be 2-5% of the total loan amount.

HELOCs

Rather than receiving your funds in a lump sum, with a HELOC from Peoples Bank you receive access to a line of credit, equal to a portion (usually 80%) of your home’s equity. This allows you to make payments on your project as needed, while only using the funds (and paying interest on those funds) that you actually need. Not only can home equity loans save you money on interest, but knowing you won’t have to make payments until you draw funds can also give some breathing room, allowing you to take the time to shop around for contractors and finalize your plans.

Use our Home Equity Line of Credit Calculator to find out how much you could qualify for, or, to learn more about HELOCs, check out our Answers to HELOC FAQs page.

Ready to Start Your Renovation?

At Peoples Bank, we can work with you to find the right financing for your home renovation project, matching your budget with your needs. A home equity loan or line of credit can help you use your home’s equity to make your home renovation dreams a reality, maximizing your renovation budget, while offering affordable, monthly payments.

Stop by one of our convenient locations to learn more about our home equity loan and line of credit options today!